Valuing Changes in Life Expectancy Part II

@ 1/16/2025 6:59:53 PM

This article is part of a two part Life Expectancy series:

Juris Economics assists practitioners making life expectancy calculations with multiple ways of entering information. There are three primary ways life expectancy calculations can be applied in our software. The first is based upon statistical tables as described in our prior blog posts. The other two are based upon witness testimony or expert opinion.

Life expectancy calculations that are based upon witness testimony or hypothetical questions require a slightly different approach. Since Juris Economics defaults to statistical calculations, we must let the software know we want to go in a different direction. This is done by selecting a “custom” life expectancy.

Juris Economics utilizes the word “custom” to signify inputs that are not based upon statistical references or reports. Accordingly, if you want to select how long a person will live based upon information provided from a witness, you must select a “Custom Life Expectancy”.

After a “Custom Life Expectancy” has been selected, a dropdown will appear. The dropdown allows a number of years to be input from the “Statistical Date of Valuation” or a specific date to be entered. These fields are interlinked. If you enter a number of years into the future, the date for the end of life expectancy will appear. Likewise, if you enter a specific date in the future, the number of years that is in the future will appear.

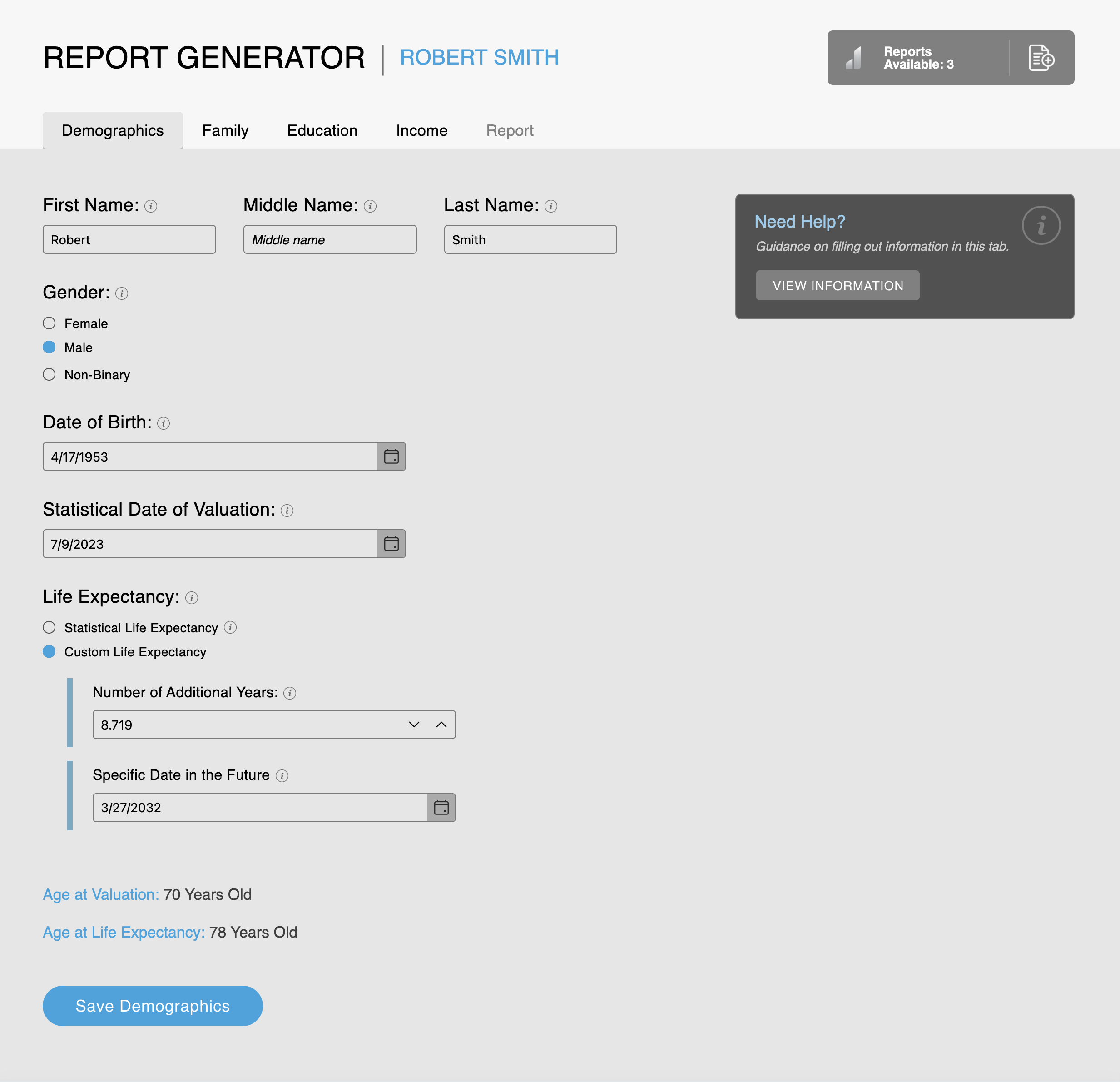

Let’s go back to our example and add some more information to this hypothetical case. The patient was a pensioner who received $120,000/year in pension benefits. He was 70 years old at the time of misdiagnosis and his normal life expectancy is 13.7 years. The physician has disclosed his malpractice policy has a limit of $1,000,000.

In order to arrive at a settlement, the patient’s lawyer wants to show what the damages are assuming the defense assertion there was a preexisting five-year life expectancy reduction. To find this number, we need to reduce the 13.7 year statistical life expectancy to an 8.7 year life expectancy.

Let’s assume the patient’s date of birth is April 17, 1953, date of misdiagnosis is July 9, 2023, and the experts have testified the patient will pass away on June 1, 2025. On the Demographics page, we switch from a statistical life expectancy of 13.7 years to 8.7 years by utilizing the “Custom Life Expectancy” option and entering 8.7. This yields an end of life expectancy of 3/27/2032.

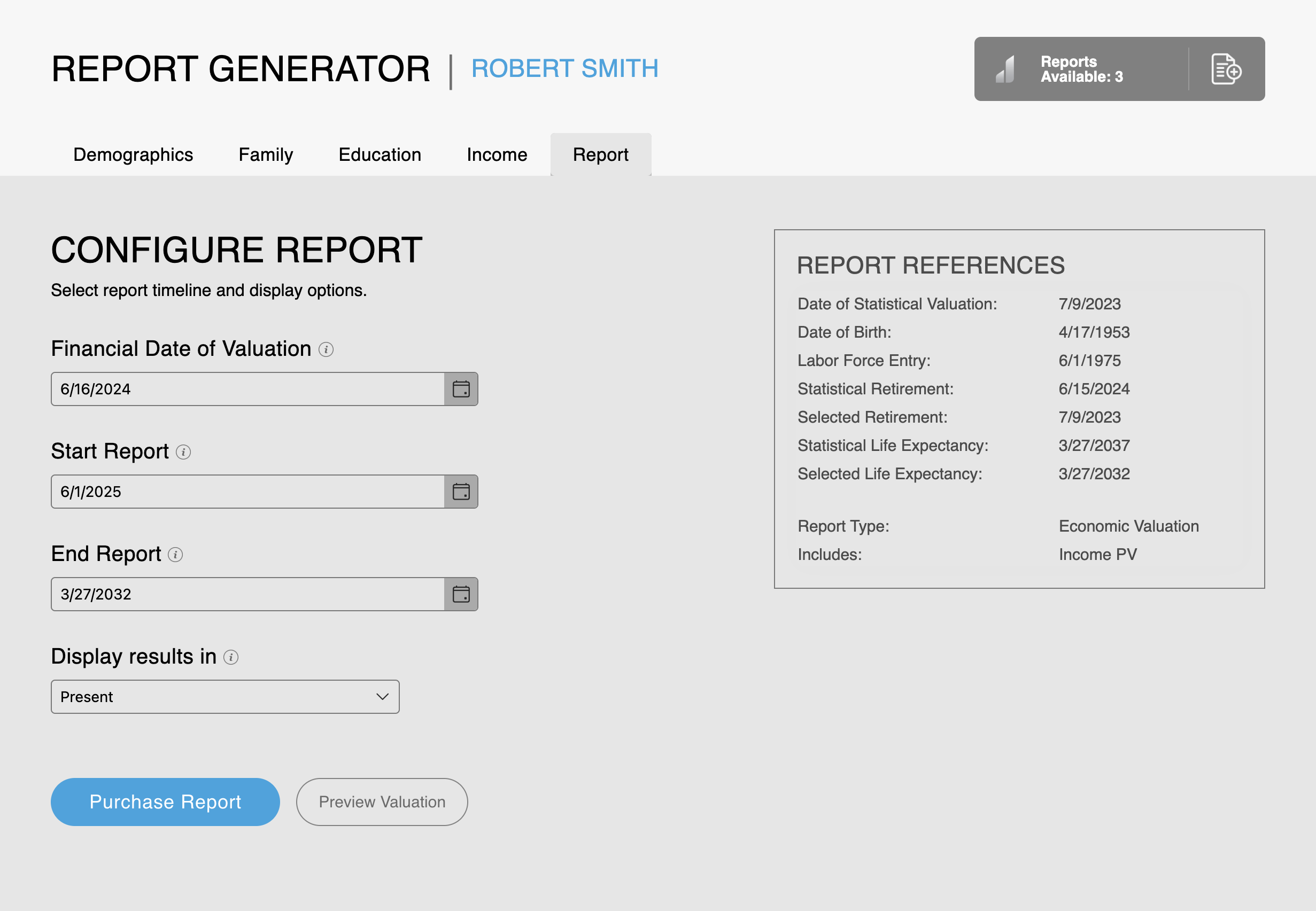

This informs us that the lost pension payments will occur from June 1, 2025 to March 27, 2032. Since there is an upcoming mediation on June 16, 2024, that will be used as the financial date of valuation. A net discount rate of 1% is also applied to get the present value. We can enter the date information on the “Report” page to ensure it is properly configured.

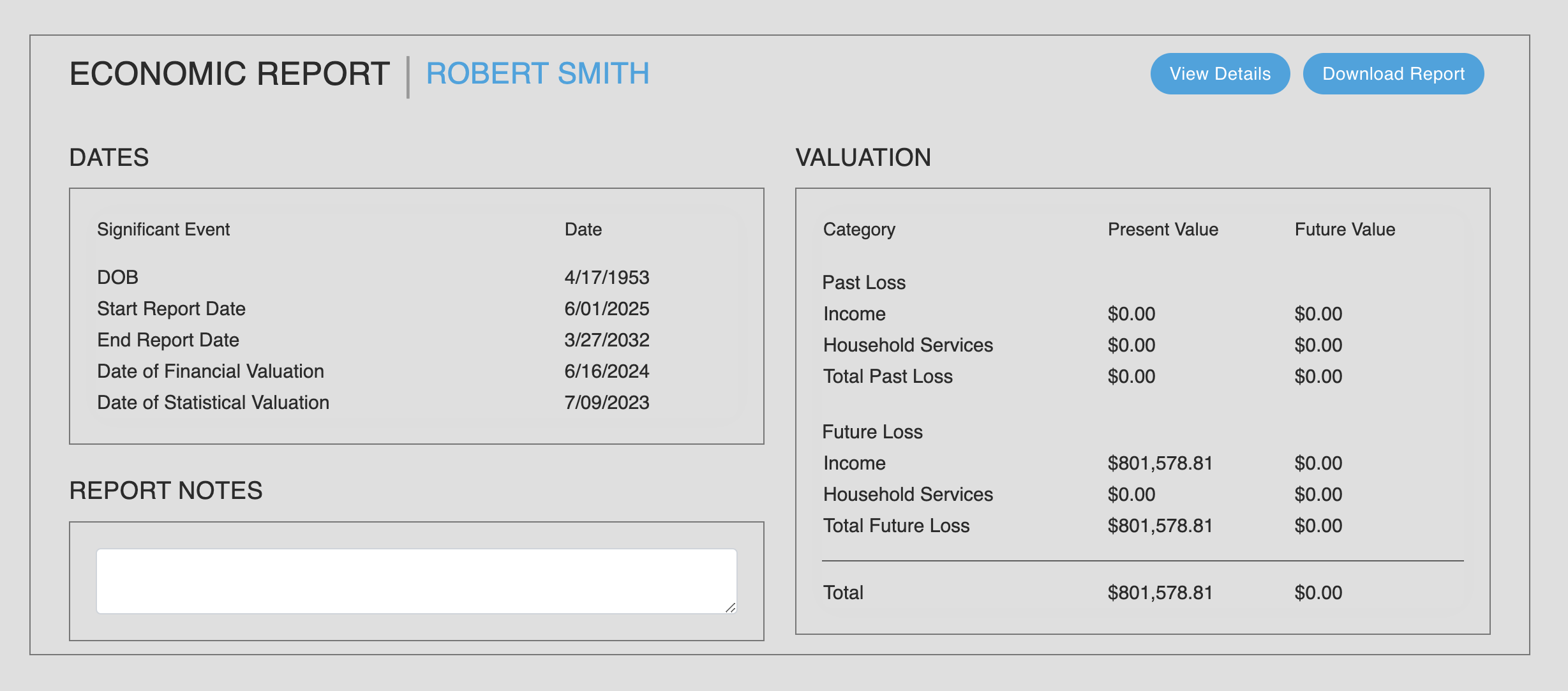

After purchasing the report, we can see the present value of the lost pension benefits amounts to $801,578.81. After presenting this information to defense counsel and taking into account pain and suffering, a policy limit settlement is reached between the parties saving time and costs for both sides.

Should you need assistance with life expectancy calculations or information, please contact Juris Economics at (858) 477-9537 or sales@juriseconomics.com

Last Modification : 1/16/2025 7:50:16 PM